To pay off credit card debt with rates near 19%, attack your highest-rate balance first while paying the minimum on the rest (the avalanche method), then cut the interest itself with a balance transfer card or a lower-rate personal loan. That combination, smaller principal plus a lower rate, is what shrinks debt fast instead of just treading water.

If you're carrying a balance right now, you already know the feeling. You pay something every month, and the number barely moves. That's not a willpower problem. That's math, and the math has been working against you.

The average credit card interest rate sat above 21% in recent reporting, according to the Federal Reserve. At those rates, a balance can grow faster than most people can chip away at it. So let's break this down into a plan you can actually run, with real numbers and honest tradeoffs.

Why 19% Interest Quietly Steals Your Money

Here's the truth most people avoid: at 19% interest, your debt has a second job, and that job is growing.

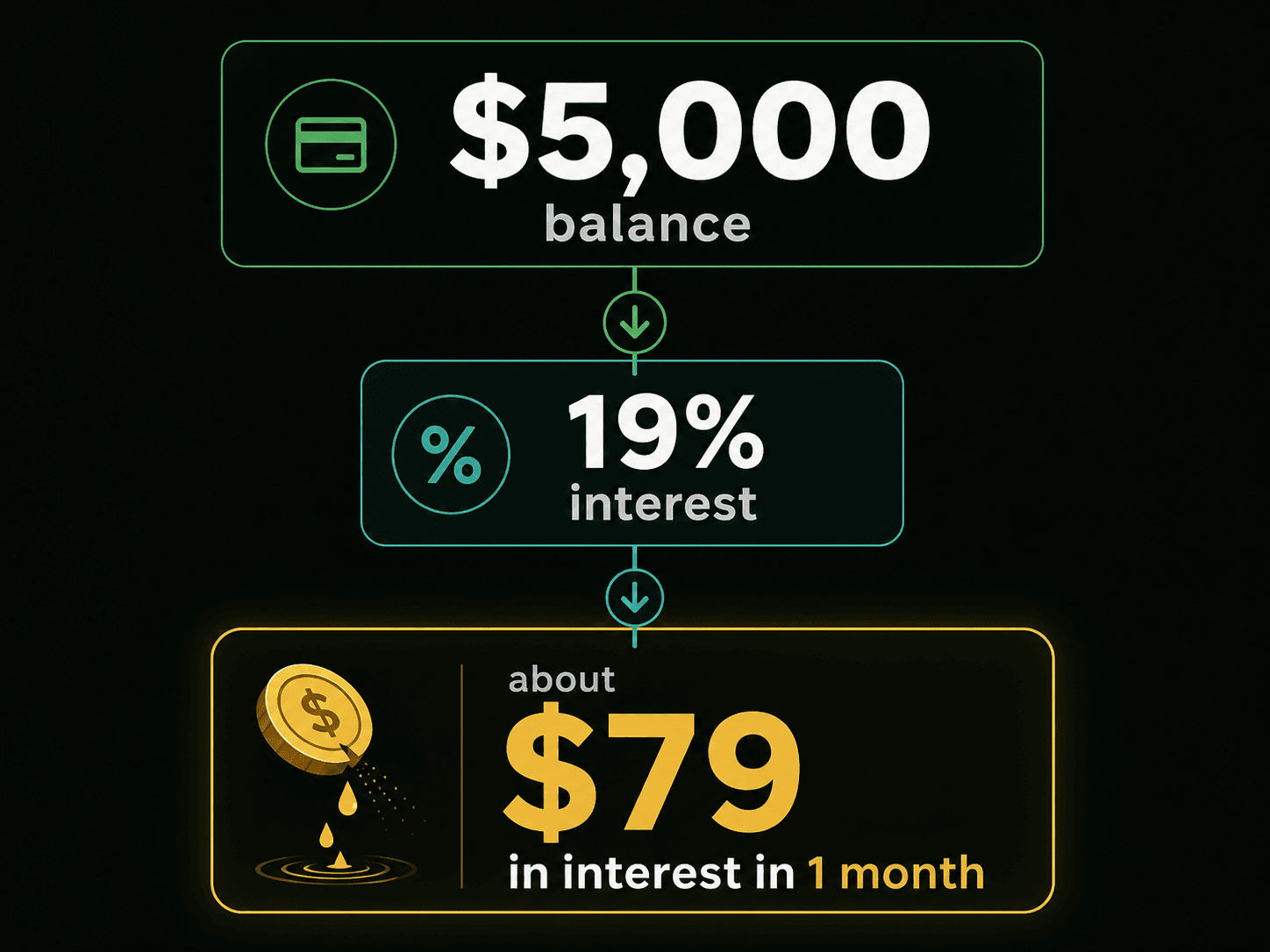

When your rate is near 19%, a $5,000 balance costs you roughly $79 in interest in a single month before you've bought anything new. Interest is the price you pay to borrow money, charged as a percentage of what you owe. The higher the rate, the more of every payment gets eaten before it ever touches what you actually borrowed.

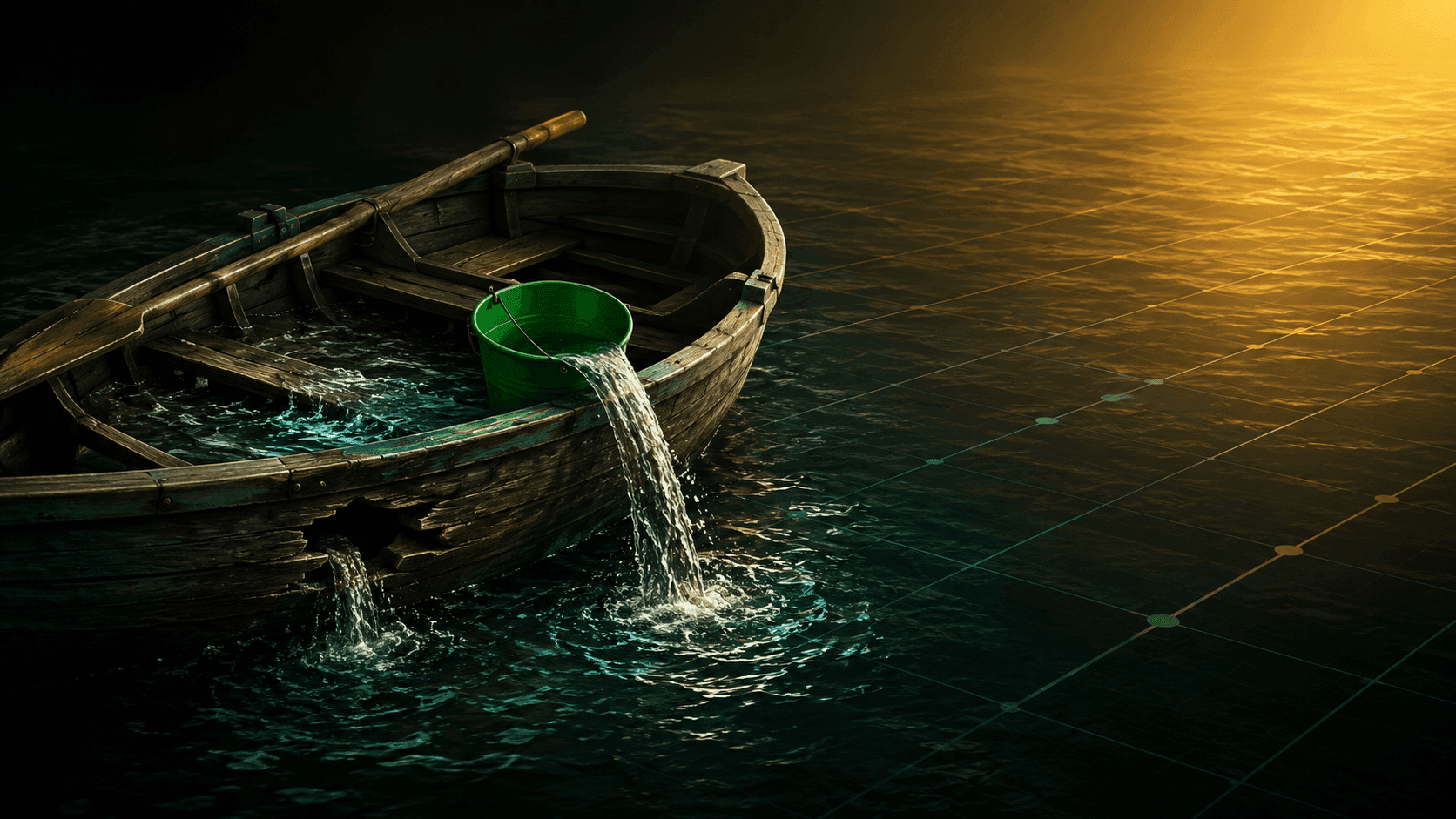

Think of it like trying to bail water out of a boat with a hole in it. You're scooping (your payments), but water keeps pouring back in (your interest). Pay only the minimum, and you're scooping just enough to stay afloat while the hole stays wide open.

That's why the first move is understanding the leak before you grab a bigger bucket.

The minimum payment trap

Minimum payments are designed to keep you in debt comfortably, not to get you out. On a $5,000 balance at 19%, paying only the minimum could stretch your payoff past 15 years and more than double what you originally owed in total interest.

The takeaway: any plan that beats the minimum is a plan worth running. Now let's pick the right one.

The Two Payoff Methods That Actually Work

Why this matters: the order you pay your cards in decides how much interest you'll hand over and how long you'll stay stuck.

There are two proven strategies, and they solve two different problems. One wins on math. One wins on motivation.

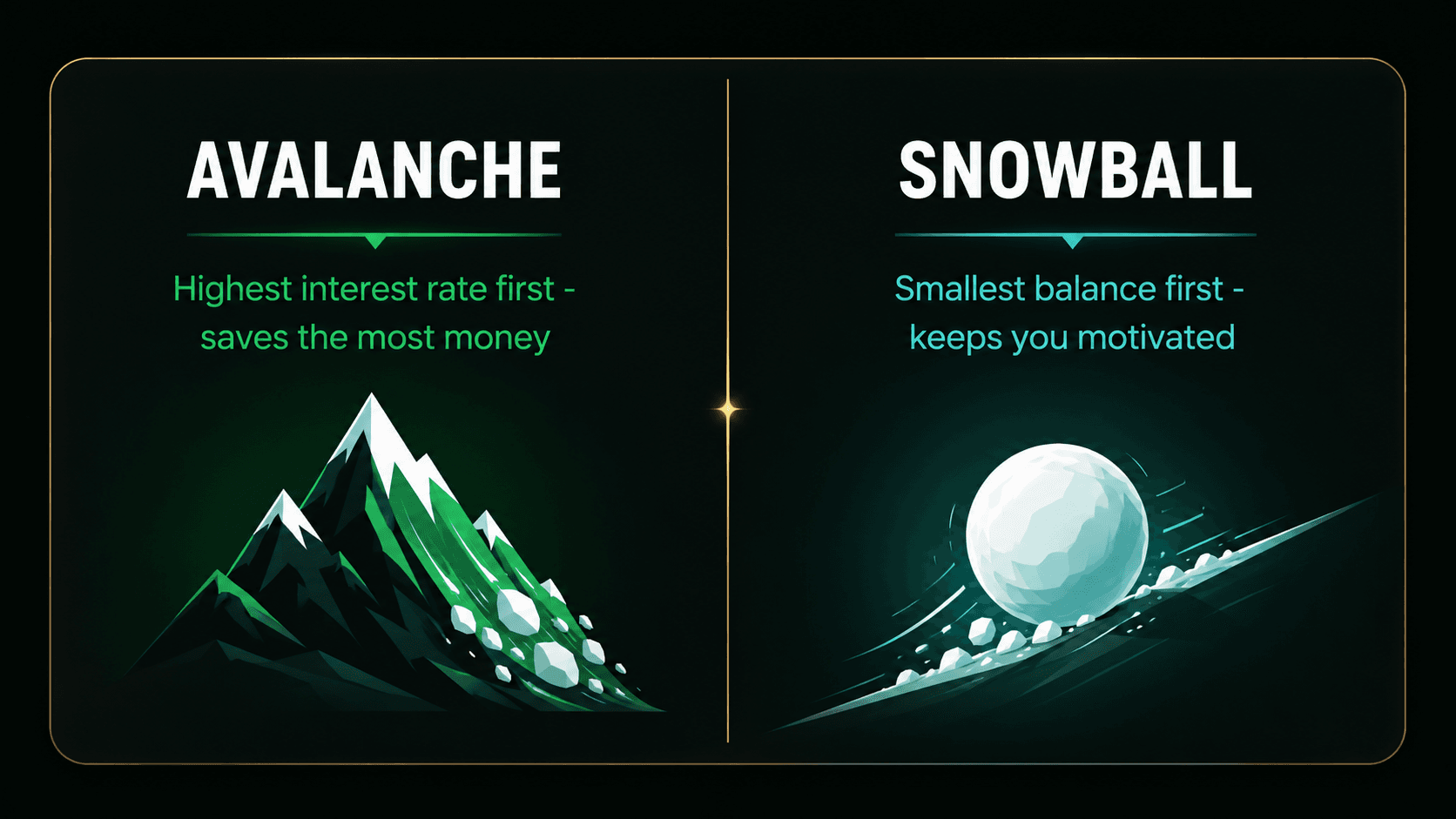

The avalanche method (cheapest)

With the avalanche, you make the minimum payment on every card, then throw every spare dollar at the card with the highest interest rate first. Once that card hits zero, you roll its payment onto the next-highest rate, and so on.

This saves you the most money because you're killing your most expensive debt first. If you have one card at 24% and one at 17%, the 24% card is the burning building. You put that fire out first.

The snowball method (most motivating)

With the snowball, you ignore rates and attack your smallest balance first, regardless of interest. Clear it, then roll that payment onto the next-smallest balance.

You'll pay slightly more in interest overall, but you get a win fast. A study published in the Journal of Marketing Research found that focusing on small balances first was the strongest predictor of actually paying down debt, because early wins keep you going.

Here's the honest decision rule. If you're disciplined and want to save the most money, run the avalanche. If you've started and quit before, run the snowball. The best method is the one you'll finish.

A quick comparison

Say you have three cards: $1,200 at 17%, $3,000 at 19%, and $800 at 26%. The avalanche tells you to kill the $800 card first (highest rate). The snowball also tells you to kill the $800 card first (smallest balance). In this case they agree, and you'd save the most by hitting that 26% card hard.

The takeaway: pick your method, list your cards in that order, and never deviate until each one hits zero.

Stop Bailing. Patch the Hole.

Let's pause, because there's a step almost everyone skips, and it quietly sabotages the whole plan.

Before you throw every dollar at debt, set aside a small starter emergency fund. Without one, the next surprise (a car repair, a vet bill) goes straight back onto the card you just paid down. You end up bailing the same water twice.

A $1,000 buffer is usually enough to keep you from reaching for plastic. We wrote a full guide on building a $1,000 emergency fund even paycheck to paycheck, and it's worth doing before you go all-in. Patch the hole, then keep bailing.

How to Pay Off Credit Card Debt at 19% Faster

Why this matters: cutting the rate itself does what no payment alone can, it shrinks the interest working against you.

The payoff method controls your principal. These tools control your rate. Used together, they're how you pay off credit card debt with rates near 19% in years instead of decades.

Option 1: A balance transfer card

A balance transfer moves your existing debt onto a new card with a 0% promotional rate, usually for 12 to 21 months. During that window, every dollar you pay goes straight to principal instead of interest.

The catch: most charge a transfer fee of 3% to 5% of the balance, and the 0% rate expires. Move $5,000 and you might pay a $150 fee, but if you'd otherwise pay 19% for a year, that's roughly $950 in interest avoided. The math usually wins, as long as you pay it off before the promo ends.

Option 2: A personal loan

A personal loan pays off your cards and replaces them with one fixed monthly payment at a lower rate, often well below 19% if your credit is decent. You trade revolving debt for a clear finish line and a set payoff date.

The tradeoff: you need to qualify, and the temptation to run the cards back up is real. The rule here is simple. The loan is a tool to escape, not a license to borrow again.

Option 3: Find extra dollars to throw at it

No new product needed. Every spare dollar you redirect to your highest-rate card is an instant 19% return, guaranteed, which beats almost any investment. Trimming your grocery bill is a great place to start, and our guide on beating inflation on groceries without coupons shows three moves that free up cash fast.

And here's a bonus move: any cash you set aside should earn while it waits. Parking your starter buffer in a high-yield savings account keeps it growing instead of sitting flat.

The takeaway: lower the rate with a transfer or loan, then feed it every extra dollar you find. Speed comes from doing both.

Your Step-by-Step Payoff Plan

Why this matters: a plan you can see is a plan you can finish.

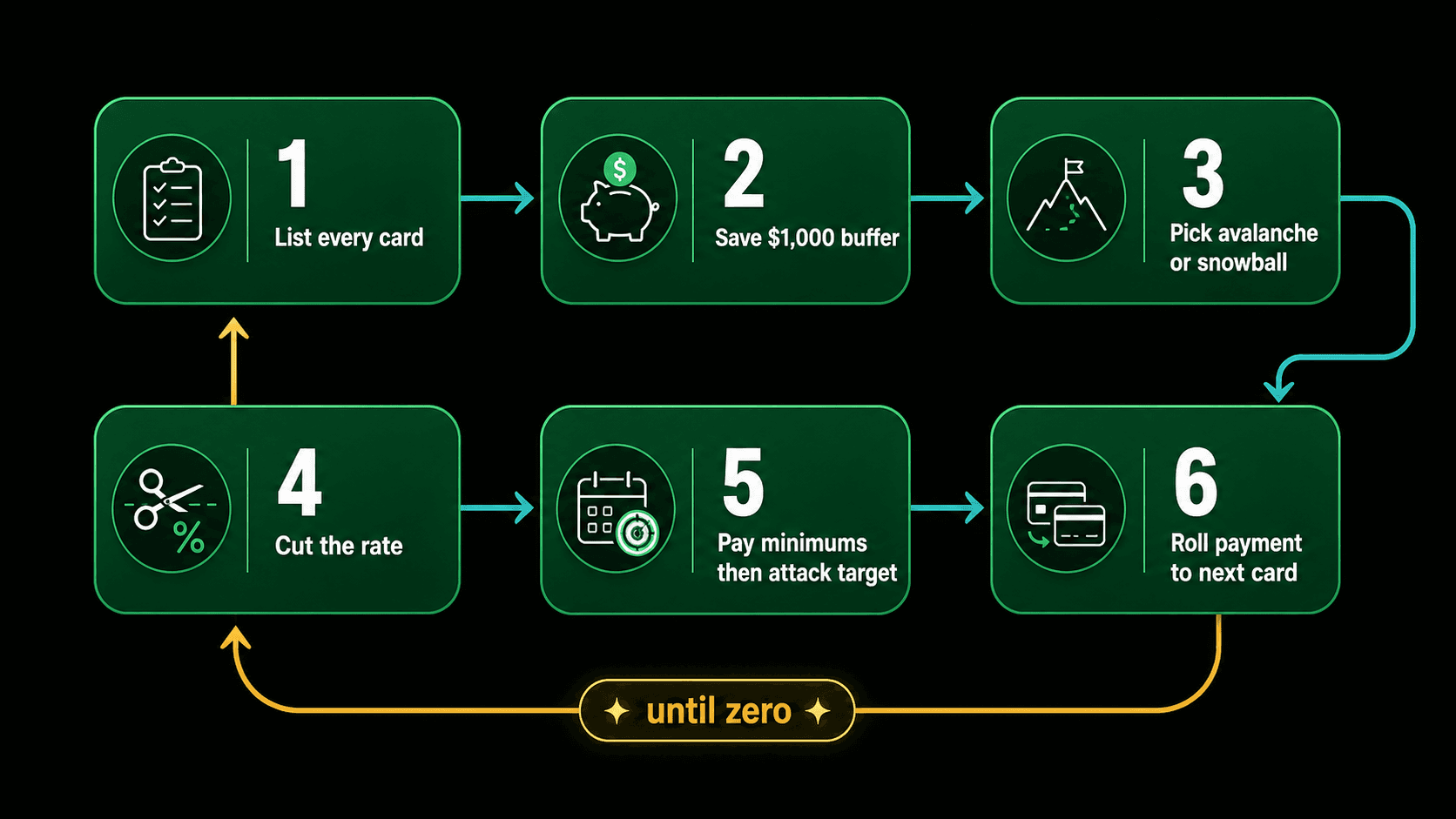

Here's the whole thing in order, start to finish:

- List every card: balance, interest rate, and minimum payment.

- Save a $1,000 starter buffer so surprises don't undo your progress.

- Pick avalanche or snowball and rank your cards in that order.

- Cut the rate with a balance transfer or personal loan if you qualify.

- Pay minimums on everything, then attack your target card with every spare dollar.

- Roll each cleared payment onto the next card and repeat until zero.

Follow that loop and the boat stops leaking. Then it starts emptying.

The takeaway: write your six steps down today and start with step one tonight.

The Bottom Line

Learning how to pay off credit card debt with rates near 19% comes down to two levers: shrink what you owe by attacking the highest-rate balance first, and shrink the rate itself with a balance transfer or a lower-rate loan. Pull both, and you stop bailing a leaky boat and start watching the water drop.

You don't need to be perfect. You need to start. Open your card statements, write down every balance and rate, and choose avalanche or snowball before you go to bed tonight. That single list is the moment your debt starts losing instead of you.