You can build a $1,000 emergency fund even if you live paycheck to paycheck. The key is starting small, automating the habit, and finding money that's already leaking from your budget without you realizing it. Most people who follow this system hit $1,000 faster than they expected.

You Are Not Alone, But You Can Change This

That feeling when a car repair bill lands or your kid spikes a fever on a Friday night? Your stomach drops before you even open your wallet. One surprise expense and the whole month unravels.

That feeling has a name: financial fragility. And it is far more common than anyone admits.

According to the Federal Reserve's 2023 Report on the Economic Well-Being of U.S. Households, 37% of Americans could not cover a $400 emergency expense without borrowing money or selling something. Not $4,000. Four hundred dollars.

If that number hit close to home, good. It means you're paying attention. And the fact that you're reading this means you're already doing something most people never do: looking for a real way out.

This guide shows you exactly how to build a $1,000 emergency fund even if your budget feels bone-dry right now. No gimmicks, no "skip your latte" lectures. Just a clear, honest system that works on a real income.

By the end, you'll know why $1,000 is the right first target, where the money is hiding in your current spending, how to automate the whole thing so it happens without willpower, and where to actually keep the fund once you build it.

Why $1,000 Is the Right First Target

The number is not random

A $1,000 emergency fund is not a full safety net. Financial experts generally recommend three to six months of living expenses for a complete emergency fund. But that number can feel so far away that most people never start.

$1,000 is the tipping point. It is enough to handle the most common financial emergencies without reaching for a credit card: a car repair, a medical copay, a broken appliance, an unexpected vet bill. Research from the Urban Institute found that families with even $250 to $749 in liquid savings were less likely to be evicted, miss a utility payment, or skip meals after a financial shock than families with no savings at all.

Think of it like a firebreak in a forest. It does not stop every fire, but it stops the small ones from becoming catastrophic.

The psychological win matters too

Hitting $1,000 rewires how you think about money. It shifts you from reactive to proactive. Once you prove to yourself that you can save, saving more becomes believable. That mindset shift is worth as much as the money itself.

Your action takeaway: Write down the number $1,000 somewhere visible. Not as a wish, as a deadline. Give yourself 90 days. That is roughly $11 a day, or $77 a week. Now let's find where that money is already hiding.

Your Money Is Leaking. Here's Where.

Small leaks sink big ships

Most people do not have an income problem. They have a leak problem. The money comes in, and it quietly disappears through a dozen small holes before you ever get a chance to save it.

Here's the truth most people avoid: you are probably spending $150 to $300 a month on things you have completely forgotten about.

Subscriptions you signed up for and never cancelled. The streaming service you share with someone but pay for alone. The gym membership that auto-renews every January. The app upgrade you clicked once. These are not moral failures. They are just invisible, and invisible spending is the enemy of saving.

The 15-minute money audit

Open your last two bank or credit card statements. Go line by line. Mark every recurring charge with an R. Then ask yourself one question for each one: "Did I consciously choose to spend this in the last 30 days?"

If the answer is no, that is a leak.

The average American spends $219 per month on subscriptions, according to a 2022 C+R Research study, but estimates they spend only $86. That gap, $133 a month, is $1,596 a year. It is also most of your $1,000 emergency fund.

Your action takeaway: Do the 15-minute audit this week. Cancel or pause anything you did not consciously choose. Redirect that money, even $30 or $50, directly into savings before you spend it on something else.

Willpower Is Not a Savings Strategy

Here is something no one tells you. The people who are great at saving are not more disciplined than you. They just built systems that remove the decision entirely.

You cannot spend money you never see. That single idea is the whole secret. Stop trying to be stronger than your impulses, and start making the smart choice the automatic one.

That's where the next move comes in.

How to Build a $1,000 Emergency Fund With Automation

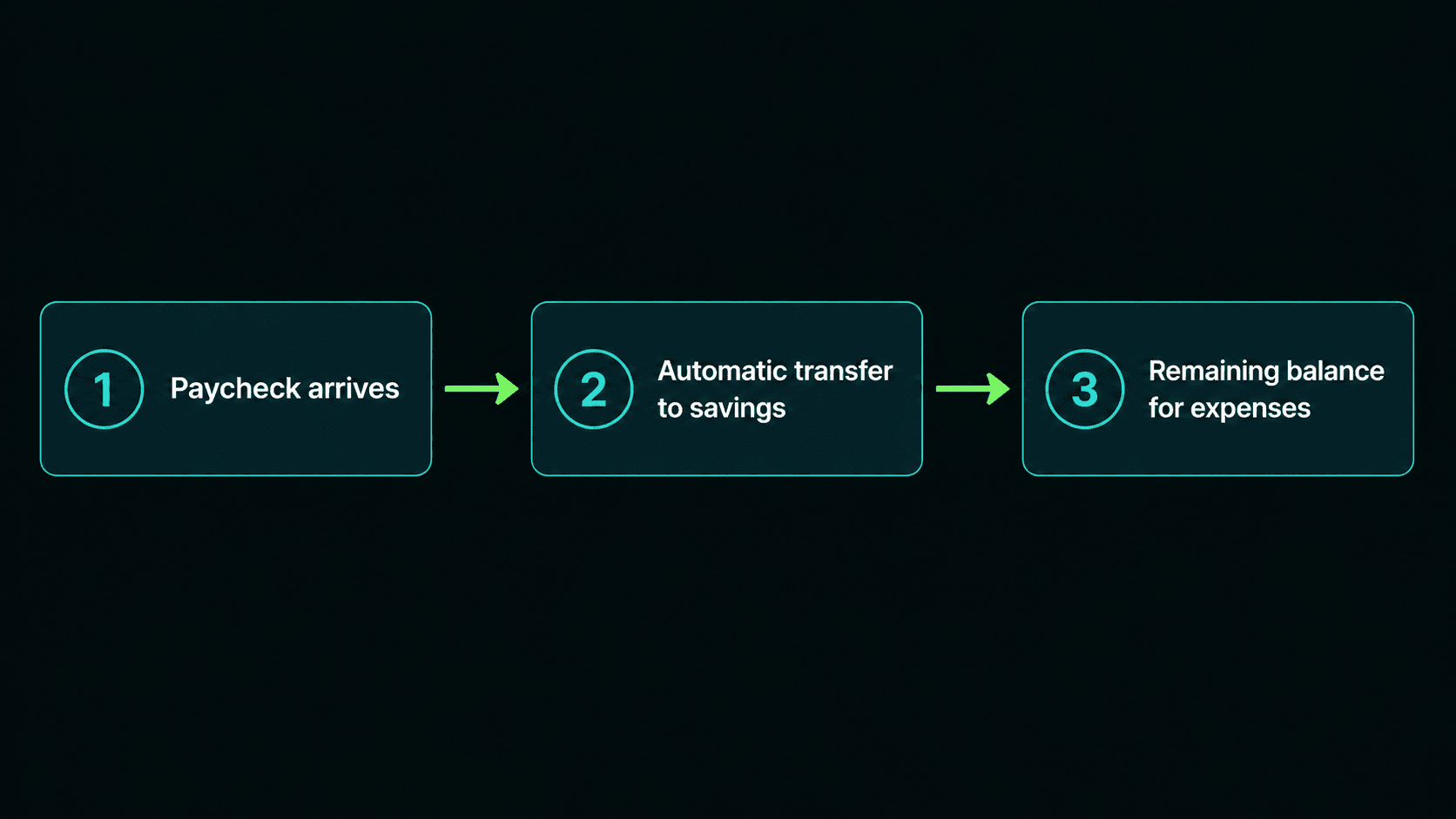

Pay yourself first

The strategy is called pay yourself first, which means treating your savings like a bill, not an afterthought. Before you pay rent, before you buy groceries, before you do anything else, a fixed amount moves into your savings account automatically.

This is the engine behind how to build a $1,000 emergency fund without relying on motivation that comes and goes.

How to set it up in three steps

-

Open a separate savings account. Not a second account at the same bank where you can transfer money back in 30 seconds. A separate account, ideally at a different institution, with a small friction barrier. Out of sight, out of mind, out of reach.

-

Set up an automatic transfer. Log into your bank and schedule a recurring transfer for the day after your paycheck hits. Start with whatever you found in the leak audit, even $25. The amount matters less than the habit.

-

Increase it by $5 every month. This is called "set it and forget it" escalation. You will not feel a $5 increase. But over six months, you will have meaningfully accelerated your savings without a single painful sacrifice.

Your action takeaway: Set up one automatic transfer today. Even $10. The goal right now is not the amount. It is the system.

What If You Genuinely Have Nothing Left After Bills?

Let's be honest with each other for a second.

Some of you are not dealing with a leak problem. You are dealing with a math problem. Income minus expenses equals zero, or worse, a negative number. And no amount of subscription-cancelling fixes that.

If that is you, this section is for you.

Building an emergency fund on low income looks different

First, reframe the goal. If $1,000 in 90 days is genuinely impossible right now, $1,000 in 180 days is not a failure. It is a plan. Progress beats perfection every single time.

Second, look for one-time income injections. A tax refund. Selling something you own but do not use. One extra shift. A small freelance job. These are not sustainable income streams, but they can give your emergency fund a jump-start that months of $10 transfers cannot.

Third, check whether you qualify for assistance programs that free up cash. SNAP benefits, utility assistance programs like LIHEAP, or local community resources can reduce your monthly expenses and create room to save. Using these programs is not a setback. It is smart resource management.

Finally, consider whether a side income is realistic, even temporarily. Delivering groceries, selling handmade items, or offering a skill you already have can add $100 to $300 a month. That alone could fund your entire emergency fund in under a year. We have a full guide on getting started with side hustles if you want to explore that path.

Your action takeaway: If your budget is truly at zero, pick one of these three moves this week: sell one unused item, check your eligibility for one assistance program, or identify one realistic way to earn an extra $50 this month.

Where to Keep Your Emergency Fund

Not all savings accounts are equal

Your emergency fund needs to be in the right place: accessible enough to use in a real emergency, but separate enough that you are not tempted to dip into it for non-emergencies.

Here is a quick breakdown of your best options:

-

High-Yield Savings Account (HYSA), best choice. A high-yield savings account works exactly like a regular savings account, except it pays significantly more interest. As of 2024, many HYSAs are offering 4% to 5% APY (annual percentage yield, the interest you earn per year), compared to the national average of 0.46% for traditional savings accounts. On $1,000, that difference is small but meaningful, and it grows as your fund grows. Look at options from SoFi, Marcus by Goldman Sachs, or Ally Bank.

-

Money Market Account, strong alternative. Similar to an HYSA, often with slightly higher minimums but comparable rates. A solid option if your bank offers one.

-

Regular Savings Account at a Separate Bank, acceptable. Not ideal for interest, but the separation from your checking account adds a friction barrier that protects the fund from impulse spending.

-

Checking account, brokerage, or cash at home, avoid. Checking accounts are too easy to spend from. Brokerage accounts can drop in value right when you need the money most. Cash at home earns nothing and carries real risk of loss.

For a deeper look at how to make your money work harder while it sits, check out our guide on how to choose the right savings account.

Your action takeaway: Open a high-yield savings account this week if you do not already have one. Most take less than 10 minutes to set up online, require no minimum deposit, and have no monthly fees.

How to Build a $1,000 Emergency Fund: Your Complete Action Plan

Here is everything you now know, pulled into one clear sequence.

$1,000 is the right first target because it handles the most common emergencies and proves to yourself that saving is possible. Your money is probably leaking through forgotten subscriptions and invisible recurring charges. Automation, not willpower, is the real savings strategy. And a high-yield savings account is where your fund belongs.

None of this requires a raise. None of it requires a perfect budget. It requires one decision, made today, followed by one small action.

If you live paycheck to paycheck, the path is the same. It may just take a little longer, and that is completely fine. Progress is progress. A $1,000 emergency fund built over six months protects you just as well as one built in three.

The single most important thing you can do right now: open a separate savings account and set up your first automatic transfer, even if it is $10. That is the whole move. Because the gap between people who build financial security and people who do not is rarely about income. It is about whether they started.

You are starting today.

Once you hit $1,000, the next step is growing your emergency fund to three to six months of expenses. Our guide on building your first complete financial safety net walks you through exactly what comes next, and what to do with money beyond that.

Open your high-yield savings account today and set up your first automatic transfer. It takes 10 minutes. Your future self will thank you for the one day you decided to start.