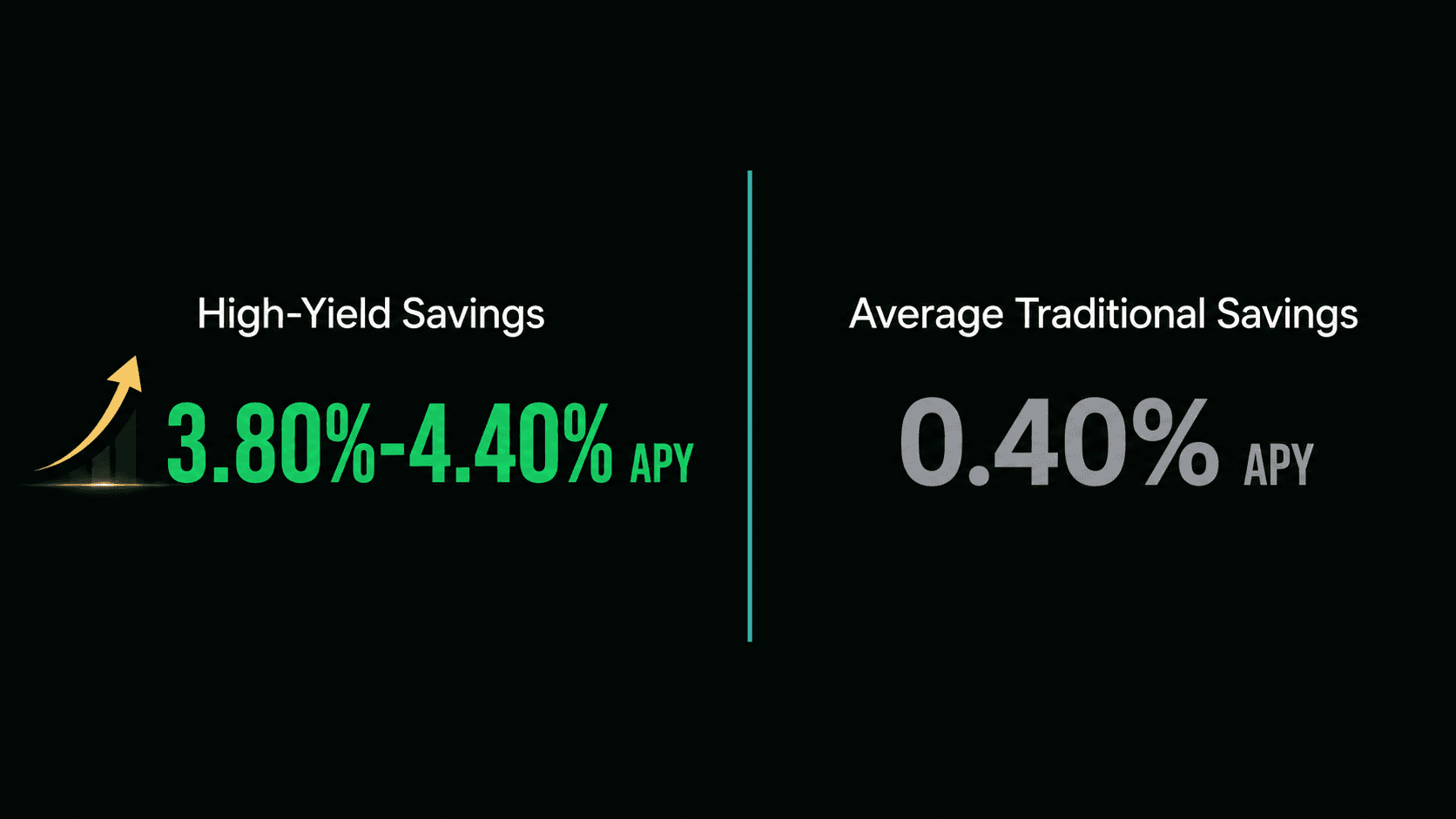

As of June 2026, the best high-yield savings account rates pay roughly 3.80% to 4.40% APY, while the average traditional savings account still pays around 0.40% APY. That gap is real money. On a $10,000 balance, the difference is about $400 a year for doing almost nothing except moving your cash to a better account.

If you're reading this, you probably suspect your money is sitting somewhere lazy. Maybe it's parked in a big-bank account you opened years ago, quietly earning pennies. You're right to be suspicious, and you're not behind. You're about to fix it in an afternoon.

Let's break down what these rates look like right now, how to tell a real deal from a bait-and-switch, and exactly how to move your money safely.

What Counts as a "Good" Rate in June 2026?

Here's the truth most people avoid: the headline number on a bank's homepage isn't the whole story. A high-yield savings account (HYSA) is simply a savings account that pays a much higher APY, or annual percentage yield, which is the real yearly return after compounding is factored in.

Right now, a competitive HYSA pays in the 3.80% to 4.40% APY range. Anything under 3% is no longer pulling its weight. Anything advertised far above 4.40% deserves a second look, because it's often a short "teaser" rate that drops after a few months.

Think of APY like the fuel efficiency rating on a car. Two cars can look identical in the showroom, but one quietly costs you more every single mile. Your savings account works the same way, except the cost is invisible until you add it up at year's end.

Your move: write down your current account's APY today. If you don't know it, that's your first red flag.

Are These Rates Actually Beating Inflation?

This matters because a number that looks big can still be shrinking your buying power. Inflation is the rate at which prices rise, which means the same dollar buys a little less each year.

When inflation cools toward the Federal Reserve's long-run 2% target, a 4% APY means your money is genuinely growing in real terms, not just on paper. You can track the official numbers through the U.S. Bureau of Labor Statistics Consumer Price Index and the Federal Reserve.

Here's the part that should light a fire under you. If inflation runs near 2% and your old account pays 0.40%, you're losing roughly 1.6% of buying power every year while feeling like you're "saving." A 4% HYSA flips that math in your favor.

Your move: compare your account's APY against the latest inflation rate. If your rate is lower, your savings are quietly melting.

How to Compare the Best High-Yield Savings Account Rates

A high APY is only the first checkbox. The best rates in June 2026 come with no monthly fees, no minimum balance to earn the rate, and FDIC or NCUA insurance.

FDIC insurance protects up to $250,000 per depositor, per bank, so your money is safe even if the bank fails. You can verify any bank's coverage directly at the FDIC's BankFind tool. Credit unions offer the same protection through the NCUA.

Walk through these five questions before you commit:

- What is the APY, and is it a teaser? Confirm whether the rate is ongoing or drops after an intro period.

- Are there fees? Monthly maintenance fees can quietly erase your gains.

- Is there a minimum balance? Some accounts only pay the top rate above a threshold.

- Is it FDIC or NCUA insured? Non-negotiable. Never skip this.

- How fast can you access your money? Check transfer times and any withdrawal limits.

Think of it like buying produce. The shiniest apple on the shelf isn't worth much if it's bruised underneath. Always check the whole fruit.

Your move: run any account you're considering through these five questions before you click "open."

Stop Chasing the Highest Number

Here's a pattern interrupt that'll save you a headache. The account with the absolute highest rate this month is rarely worth chasing if it means hopping banks every 90 days.

Rate-chasing feels productive, but it's busywork dressed up as strategy. The difference between a 4.10% and a 4.25% APY on $10,000 is about $15 a year. That's not worth re-linking accounts, updating direct deposits, and tracking another login.

Pick a reputable account in the top tier and stay put. Consistency beats optimization here, the same way showing up to the gym beats the perfect workout plan you never start.

How to Move Your Money in One Afternoon

This is where most people stall, so let's make it painless. Switching to a high-yield savings account is a short, repeatable process, not a financial overhaul.

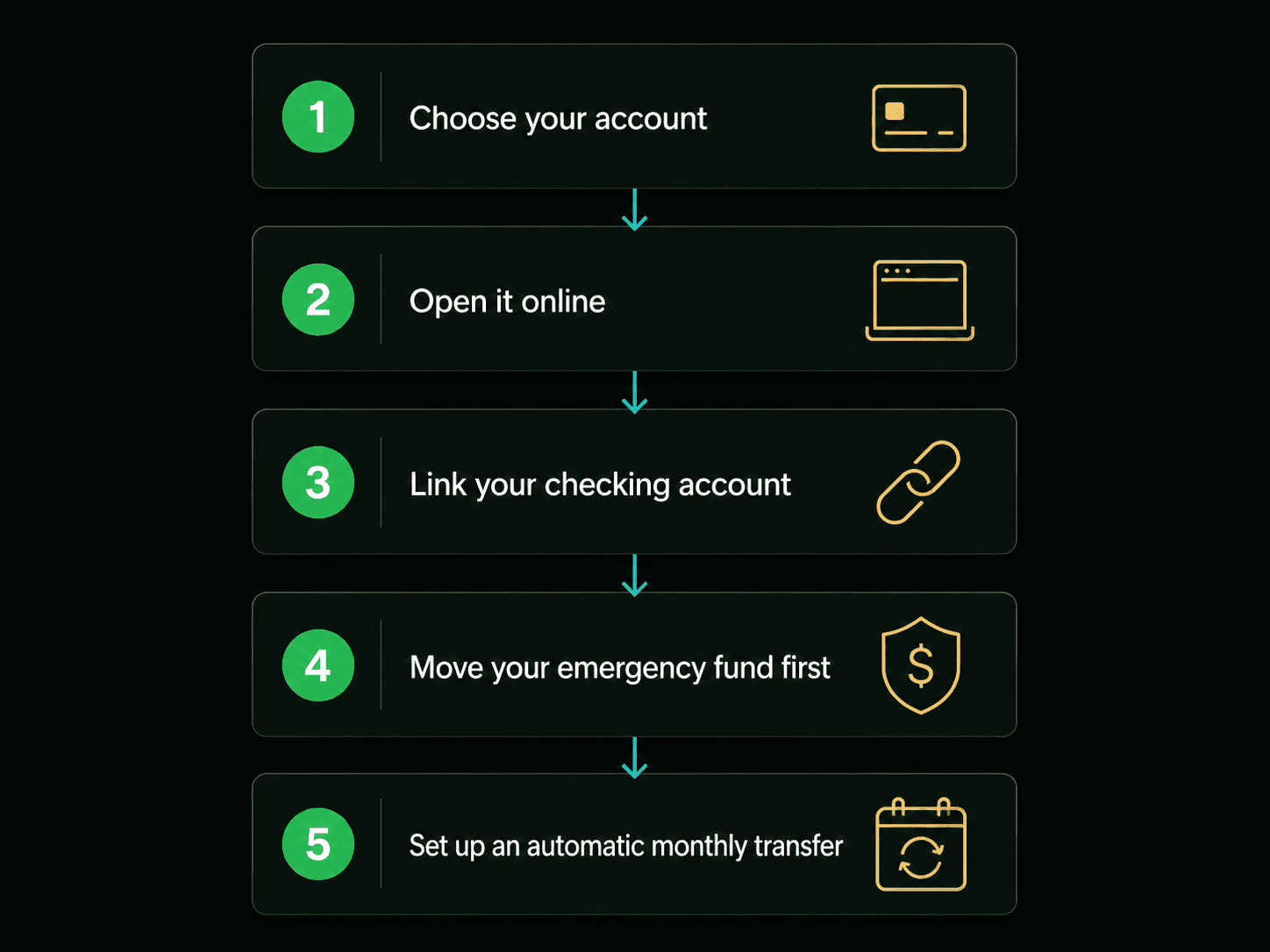

Follow these steps in order:

- Choose your account using the five questions above.

- Open it online, which usually takes 10 to 15 minutes and your ID plus Social Security number.

- Link your existing checking account to enable transfers.

- Move your emergency fund first, since that cash should be earning the most while staying liquid.

- Set up an automatic monthly transfer, even $50, so saving happens without willpower.

Keep your old checking account if you like it. The goal isn't to burn everything down, just to stop letting your savings sit idle. If you don't have an emergency fund yet, start with our guide on building an emergency fund from zero, then pair it with a system from our simple budgeting framework.

Your move: block 30 minutes this week and open the account. Future-you will quietly thank present-you every month.

Where a HYSA Fits in the Bigger Picture

A high-yield savings account is a fantastic tool, but it's a tool, not the whole toolbox. It's built for money you might need within a few years: your emergency fund, a house down payment, a planned big purchase.

For money you won't touch for a decade or more, a savings account isn't enough. That's where long-term growth comes in, because even 4% can't match the historical returns of broad market investing over time. When you're ready for that step, our walkthrough on how to start investing as a beginner is the natural next move.

Think of your HYSA as the safe, sturdy foundation and investing as the house you build on top. You need both, in the right order.

Your move: decide which dollars are short-term (HYSA) and which are long-term (investing). Clarity here prevents costly mistakes later.

The Bottom Line on the Best High-Yield Savings Account Rates in June 2026

The best high-yield savings account rates in June 2026 sit around 3.80% to 4.40% APY, roughly 10 times what a traditional savings account pays. On a $10,000 balance, switching can mean about $400 a year, with no extra risk and no extra effort once it's set up.

You don't need the single highest rate. You need a fee-free, FDIC-insured account in the top tier, and the discipline to move your money once and leave it alone. The strategy is simple. The hard part is just starting.

So do the small thing today: check your current APY, then open a better account this week. Your money should be working as hard as you do.