With the SAVE plan ending, here's how to choose a new student loan repayment plan in one sitting: compare the remaining income-driven plans (IBR, PAYE, and ICR) against the Standard plan, then pick the one that keeps your monthly payment affordable while protecting any forgiveness progress you've already earned. For most borrowers carrying high balances on modest incomes, an income-driven plan still wins. For those close to paying off, the Standard plan usually costs less overall.

If you were enrolled in SAVE, you've probably felt that pit-in-your-stomach uncertainty. Your payment was paused, the rules kept shifting, and now you're being told to choose again. That's exhausting. Let's take the fear out of it and turn this into a decision you can actually make in an afternoon.

What Happened to the SAVE Plan, Plainly

Here's the truth most headlines skip. The SAVE plan (Saving on a Valuable Education) was an income-driven repayment plan that lowered payments and stopped interest from snowballing. After federal court challenges, it was blocked and is being wound down, which means borrowers enrolled in it have to move to a different plan.

An income-driven repayment plan, or IDR, simply ties your monthly payment to what you earn instead of what you owe. Think of it like rent based on your paycheck rather than the size of the apartment. When your income is low, your payment is low.

While SAVE borrowers were in forbearance, no payments were due, but for a stretch that time didn't count toward forgiveness. According to the U.S. Department of Education, borrowers will need to enroll in a new plan to resume progress. Knowing that timeline matters, because waiting too long can cost you.

That's the setup. Now let's figure out which door you should walk through.

Your Real Options Now That SAVE Is Ending

Why this matters: the wrong plan can quietly cost you thousands in extra interest or push back your forgiveness date by years. The right one fits your income today and your goal tomorrow.

You have four main paths. Each works differently depending on your balance, your income, and how close you are to the finish line.

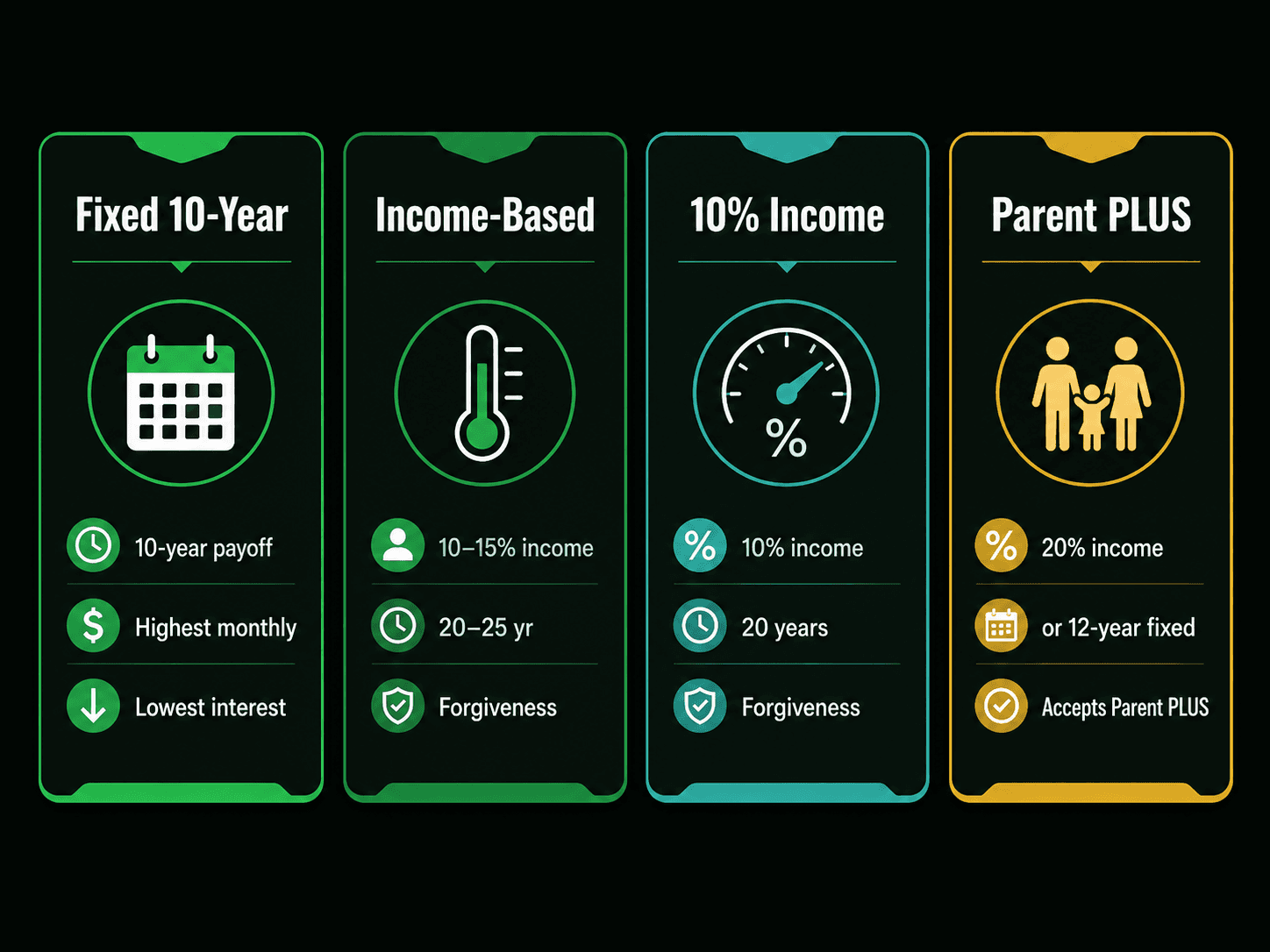

The Standard Repayment Plan

This is the default. You pay a fixed amount over 10 years, and your loan is gone fastest with the least total interest. The catch is the monthly payment is the highest, because it's based on your balance, not your paycheck.

Think of it like paying off a car loan on a strict schedule. It stings monthly, but you own it sooner and pay less overall. If your income comfortably covers it, this is often the cheapest route.

Income-Based Repayment (IBR)

IBR caps your payment at 10% or 15% of your discretionary income (the money left after basic living costs), depending on when you borrowed. After 20 or 25 years of qualifying payments, the remaining balance can be forgiven.

Imagine a thermostat that adjusts to the room. Earn less, pay less. IBR is a strong landing spot for SAVE borrowers because it's protected by law, not just policy, so it's far less likely to vanish overnight.

Pay As You Earn (PAYE) and Income-Contingent Repayment (ICR)

PAYE caps payments at 10% of discretionary income with forgiveness after 20 years. ICR is less generous, using 20% of discretionary income or a 12-year fixed schedule, whichever is lower. ICR is the only IDR plan that accepts Parent PLUS loans once they're consolidated.

The takeaway: if you qualify for PAYE, it usually beats ICR. Use ICR mainly when nothing else fits.

Stop Refreshing Your Loan Portal at Midnight

Let's be honest. The anxiety here isn't really about percentages. It's the feeling that the rules keep changing and you're somehow falling behind through no fault of your own.

You're not behind. You're adapting to a system that moved the goalposts, and the fact that you're reading this means you're already ahead of most borrowers who are ignoring the letters entirely. Breathe. This is a paperwork problem, not a character flaw.

One decision, made calmly, fixes most of it. Let's build that decision now.

How to Choose a New Student Loan Repayment Plan

Why this matters: choosing by guesswork is how people end up overpaying. Choosing by a simple set of rules is how you keep more money and your sanity.

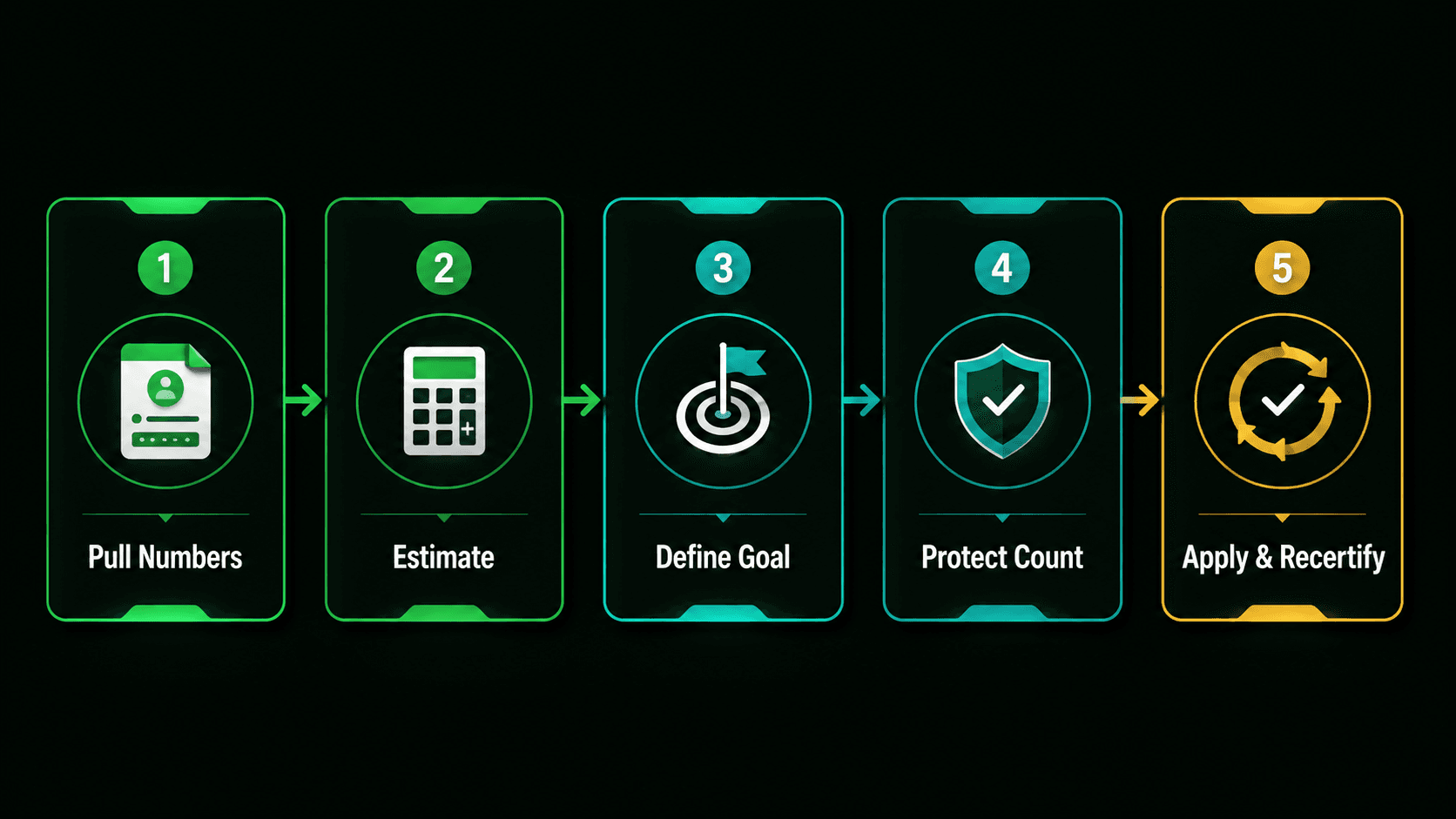

Here's a clean process you can run in one sitting.

- Pull your numbers. Log in to your loan servicer and note your total balance, interest rate, and loan type. Federal Direct loans qualify for every plan; older FFEL loans may need consolidating first.

- Estimate your payments. Use the official Loan Simulator at StudentAid.gov to compare your monthly cost under each plan side by side.

- Define your goal. Are you chasing the lowest monthly payment, the lowest total cost, or Public Service Loan Forgiveness? Your goal decides the winner.

- Protect your forgiveness count. If you've made years of qualifying payments, pick an IDR plan that preserves them. Switching to Standard can interrupt that progress.

- Apply and recertify. Submit the IDR application, then mark your calendar to recertify your income every year so your payment stays accurate.

A Quick Decision Rule

If you're going for forgiveness or your income is tight, choose IBR or PAYE. If you can afford it and want to be debt-free fastest, choose Standard. If you have Parent PLUS loans, consolidate and use ICR. That's the whole map.

For a friendly example: say you owe $42,000 at a $48,000 salary. Standard might run around $450 a month, while an income-driven plan could land near $250. If money is tight, that $200 gap is groceries and breathing room. If it isn't, Standard saves you years of interest.

Want to go deeper on cutting interest while you repay? Our guide on paying off debt faster pairs perfectly with whichever plan you pick.

Mistakes That Cost SAVE Borrowers the Most

Why this matters: the plan you choose is only half the battle. The other half is avoiding the small errors that quietly add zeros.

The most expensive mistake is doing nothing. If you ignore the transition, you risk being placed on a default plan that doesn't match your income or, worse, missing payments once forbearance ends. Inaction is a decision, and it's usually the wrong one.

The second is letting interest capitalize. When unpaid interest gets added to your principal, you start paying interest on interest, the snowball rolling the wrong way downhill. Recertifying on time and staying enrolled keeps that snowball small.

The third is forgetting to recertify income annually. Skip it, and your payment can jump to the Standard amount overnight. Set a yearly reminder. That one habit protects everything else.

If building reliable money habits is your weak spot, our take on money habits that build wealth will reinforce this nicely.

Your Next Move

The SAVE plan ending isn't a crisis, it's a fork in the road, and now you know how to choose a new student loan repayment plan with clear eyes. Match the plan to your goal: IBR or PAYE for affordability and forgiveness, Standard for the fastest payoff, ICR for Parent PLUS loans. Then recertify every year and never let inaction make the choice for you.

Open the official Loan Simulator at StudentAid.gov today, run your numbers under each plan, and enroll in the one that fits the life you're actually living. One afternoon now buys you years of calm later.